Solid Oxide Fuel Cells 2026: How Data Center Demand Unlocked Commercial Scale

From Pilot to Powerhouse: SOFC Adoption Shifts to Commercial Deployments

Solid Oxide Fuel Cell (SOFC) adoption has pivoted from broad, pilot-scale validation across multiple sectors to focused, large-scale commercial deployment, driven primarily by the data center industry’s demand for clean, grid-independent power. The period between 2021 and 2024 was defined by projects aimed at proving the technology’s viability in new environments. The current 2025-2026 cycle, however, is characterized by the execution of commercially-financed, multi-megawatt projects that treat SOFCs as a bankable solution for mission-critical infrastructure.

- Between 2021 and 2024, industry activity centered on validation through pilot projects. Key examples include the Shell-led consortium to test SOFCs for maritime propulsion and Denso’s project using SOFCs for energy management at a manufacturing plant. These initiatives were essential for de-risking the technology in real-world operational settings.

- The market’s focus shifted decisively in 2025-2026 toward commercial scale. This change is best exemplified by Day One Data Centers’ announcement in January 2026 of a $2 billion+ funding round to construct facilities, including a 20-megawatt SOFC-powered data center in Singapore. This project moves the technology from a proof-of-concept to a primary power source for critical digital infrastructure.

- While the primary commercial driver has become large stationary power, the application range continues to diversify. Startups like Galt Tec, which raised €1 million in February 2025 for micro-tubular SOFCs, are targeting portable power niches. This demonstrates a healthy innovation ecosystem developing alongside the massive deployments in the data center sector.

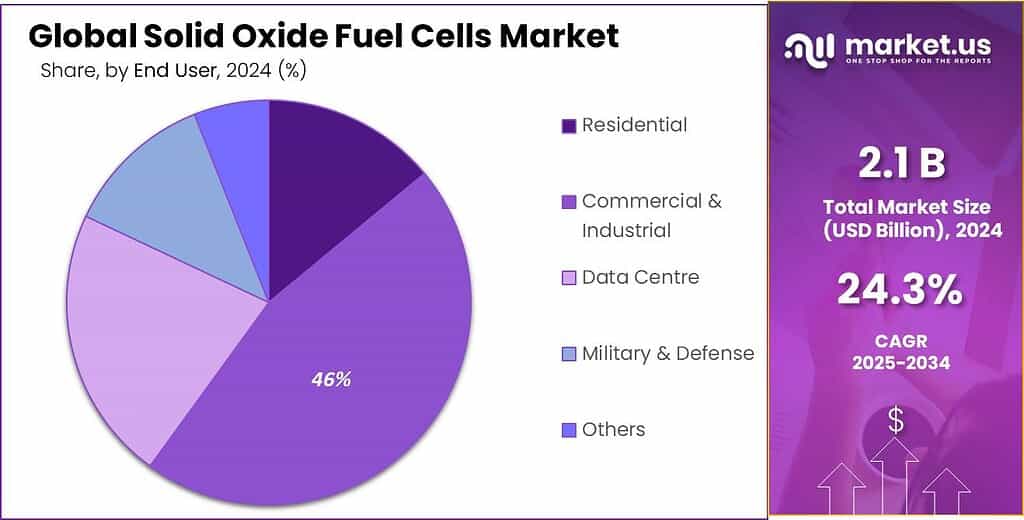

Commercial Sector Dominates 2024 SOFC Market

This chart validates the section’s premise by showing that in 2024, Commercial & Industrial applications already accounted for the largest market share, marking the shift from pilot-scale to commercial focus.

(Source: Market.us)

Investment Skyrockets: SOFC Market Attracts Multi-Billion-Dollar Project Finance

Investment in the Solid Oxide Fuel Cell sector has escalated dramatically, shifting from the early-stage and pilot funding seen before 2025 to multi-billion-dollar project finance for commercial deployments. This influx of large-scale capital, particularly in 2026, confirms growing investor confidence in the technology’s bankability for major infrastructure projects, especially as a hedge against energy supply volatility. The need for resilient power is underscored by growing geopolitical instability, which creates significant risks for data centers reliant on traditional energy grids.

SOFC Market to Explode Past $5B in 2026

The chart’s projection of explosive growth, with a specific forecast of $5.05 billion for 2026, directly visualizes the “investment skyrockets” and multi-billion-dollar project financing described in the section.

(Source: Fortune Business Insights)

- The $2 billion+ Series C funding secured by Day One Data Centers in January 2026 marks a significant change in investment scale. This capital is not for research but for the direct construction of commercial assets, signaling that private markets now view SOFC technology as a mature and deployable solution.

- A healthy early-stage ecosystem continues to thrive, validating niche applications. In November 2025, Power UP Energy Technologies secured a €10 million Series A round to manufacture specialized power units, while Galt Tec raised €1 million for its micro-SOFC technology, showing that innovation is occurring at both ends of the market spectrum.

- The scale of capital contrasts sharply with the pre-2025 period. Earlier years focused on corporate R&D and strategic partnerships to develop technology. The current environment is defined by the arrival of large-scale project finance to execute on the technology that was previously validated.

Table: Key Investments and Funding in the SOFC Sector (2025-2026)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Day One Data Centers Ltd. | Jan 2026 | Secured over $2 Billion in Series C funding to finance data center construction, including a 20 MW SOFC-powered facility in Singapore, confirming commercial bankability. | Silicon Angle |

| Power UP Energy Technologies | Nov 2025 | Raised €10 Million in a Series A round to accelerate manufacturing of its portable and specialized power units for high-reliability markets. | EU-Startups |

| UK Government | Jul 2025 | Granted £63 Million from the Advanced Fuels Fund to 17 UK companies developing sustainable aviation fuel, an ecosystem that can create fuel sources for SOFCs. | UK Department for Transport |

| Galt Tec | Feb 2025 | Raised €1 Million in a pre-seed funding round to advance its micro-tubular SOFCs for portable and off-grid power solutions. | Vestbee |

Strategic Alliances Mature to Support Manufacturing Scale

Strategic partnerships in the SOFC sector have matured from technology validation consortiums to supply-chain-focused alliances designed to enable mass manufacturing and large-scale project execution. Before 2025, collaborations were primarily structured to prove SOFCs could work in new applications. Now, the focus is on building a robust supply chain to deliver the hardware for the multi-megawatt projects being financed, especially as energy security concerns drive a re-evaluation of dependencies on traditional fuels like LNG as a transition fuel.

- The 2022-2024 period was defined by foundational partnerships aimed at de-risking technology. This includes the Shell-led consortium with Ceres Power and Wärtsilä to prove maritime viability and Ceres’ licensing deals with industrial giants Bosch and Weichai Power to prepare for mass manufacturing.

- By 2025, the market’s priority shifted toward securing the supply of core components. The investor interest shown in Elcogen’s new high-volume cell and stack factory in Tallinn signals that the key challenge is no longer just technology validation but manufacturing capacity.

- The partnership between data center operator Day One and its undisclosed SOFC supplier for a 20 MW project represents the new model: a direct commercial relationship between an end-user and a technology provider to execute a large-scale deployment, moving beyond the exploratory consortiums of the past.

Table: Evolution of Strategic SOFC Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Elcogen / Investment Groups | 2025 | Elcogen’s new high-volume SOFC and SOEC plant in Tallinn attracted visits from investment groups, signaling a market shift toward securing manufacturing capacity. | London Stock Exchange |

| Ceres Power / HUB Security | May 2023 | Initiated a pilot project to integrate SOFC technology into data center solutions, validating the application for critical digital infrastructure. | [PDF] Ceres Power |

| Shell / Ceres / Wärtsilä | Oct 2022 | Formed a consortium to trial SOFC technology as a scalable propulsion solution for the shipping sector, aimed at proving technology in a new vertical. | Shell |

| Bloom Energy / Baker Hughes | Pre-2025 | A partnership to explore integrated solutions combining Bloom’s SOFC technology with Baker Hughes’ energy technology expertise for decarbonization. | Internal Analysis |

Estonia Rises as an Innovation Hub Amid Global Deployment

While Europe, particularly Estonia, has emerged as a hub for SOFC technology innovation and startup activity, large-scale project finance and deployment are becoming globally distributed. North America and Asia Pacific are now attracting significant capital for data center and industrial applications. Before 2025, activity was concentrated in established markets, but the current period shows a more diversified geographic footprint for both innovation and commercialization, reflecting a broader global energy transition.

Asia-Pacific Emerges as a Key Growth Driver

This chart supports the section’s theme of global deployment by identifying the Asia-Pacific region as the largest and fastest-growing market, confirming that commercialization is globally distributed.

(Source: MarketsandMarkets)

- In the 2021-2024 period, North America was a key market for established players like Bloom Energy, while industrial and licensing activities were prominent in Japan (Denso) and Europe (Ceres, Bosch). The US Inflation Reduction Act provided a significant policy tailwind.

- The 2025-2026 timeframe has highlighted Estonia as a center of SOFC innovation. A cluster of companies including Elcogen (high-volume manufacturing), Galt Tec (micro-SOFCs), and Power UP Energy Technologies (specialized units) are all based in Tallinn.

- However, the largest commercial projects are global. The landmark 20 MW SOFC-powered data center project by Day One is located in Singapore, demonstrating Asia’s role as a key deployment market. This confirms that while innovation may be clustered, deployment follows the demand for reliable power in critical economic hubs.

SOFC Technology Reaches Commercial Maturity for Critical Power

Solid Oxide Fuel Cell technology has decisively transitioned from a pilot-stage solution to a commercially mature power source for specific high-value applications. The technology’s core value propositions, including high electrical efficiency and fuel flexibility, are no longer just research goals but are now validated in real-world, large-scale deployments. This maturity is critical for decarbonization efforts across multiple sectors, including challenging areas like Direct Air Capture (DAC) which require vast amounts of clean, reliable energy.

Rising Installations Prove Commercial Maturity

The chart provides direct evidence of commercial maturity by showing a significant upward trend in annual installations (MW) and identifying Commercial and Data Center segments as key applications.

(Source: IDTechEx)

- Prior to 2025, technology maturity was demonstrated through pilot success and technical announcements, such as Bloom Energy achieving 60% electrical efficiency. Performance benchmarks, like combined heat and power (CHP) efficiency reaching up to 90%, were established in controlled settings.

- In 2025-2026, maturity is confirmed by bankability. The $2 billion+ investment into Day One’s SOFC-powered data center shows the technology is now considered a reliable and economically viable solution for mission-critical infrastructure, moving beyond theoretical benchmarks to commercial reality.

- Key performance indicators are now established industry standards. SOFCs consistently offer electrical efficiencies over 60%, total system efficiency near 90% in CHP mode, and the proven flexibility to run on natural gas, hydrogen, biogas, and ammonia.

SWOT Analysis: SOFCs Capitalize on Efficiency as Costs Become Manageable

The SOFC market has successfully converted its primary weakness, high capital cost, into a manageable risk for specific high-value sectors like data centers that prioritize power reliability. The technology’s core strength of high efficiency has been validated at a commercial scale, opening new market opportunities and solidifying its role in a decarbonizing global economy where energy supply chains are under constant stress.

- Strengths have been validated and enhanced, moving from lab-based claims to commercially proven performance at the multi-megawatt scale.

- Weaknesses like high capital cost remain, but are being mitigated by manufacturing scale and accepted by customers who need uninterruptible power.

- Opportunities have crystallized around the data center market, which has emerged as the primary commercial driver, superseding the more exploratory pilots in other sectors.

- Threats from alternative technologies persist, but the threat of grid instability has ironically become a powerful driver for SOFC adoption.

Table: SWOT Analysis for the Solid Oxide Fuel Cell Market (2021-2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency (>60%) and fuel flexibility (natural gas, hydrogen) demonstrated in pilots. Licensing models (Ceres) enabled asset-light scaling. | Efficiency and reliability are proven at commercial scale (Day One’s 20 MW project). Fuel flexibility expanded to include ammonia with high efficiency (~65%). | The core value proposition of high efficiency was validated in bankable, large-scale commercial projects, moving from a technical specification to a key economic driver. |

| Weaknesses | High upfront capital cost was a major barrier to widespread adoption. Manufacturing was not yet at a scale to significantly reduce costs. | Capital cost remains high but is now acceptable for high-value applications like data centers. Manufacturing scale emerges as the new competitive frontier (e.g., Elcogen). | The high-cost weakness was reframed as a manageable premium for reliability in a specific, high-growth market (data centers), effectively de-risking it for investors. |

| Opportunities | Emerging applications in maritime (Shell trial) and data centers (Ceres/HUB pilot). The US Inflation Reduction Act created a powerful policy incentive. | The data center market became the primary commercial driver, evidenced by Day One’s $2 B+ funding. Niche markets (portable power) gain traction (Galt Tec, Power UP). | The “data center gold rush” became the definitive market opportunity, attracting massive capital and confirming SOFCs as a key enabling technology for the AI boom. |

| Threats | Competition from other clean technologies and the falling cost of renewable energy plus storage. Grid electricity was a cheaper alternative. | Grid instability and geopolitical energy risks have become a threat to traditional power models, turning a former SOFC weakness into an advantage. Competition remains, but SOFCs’ on-site reliability is a unique selling point. | The external threat of grid unreliability became a primary driver for SOFC adoption, fundamentally shifting the competitive dynamic in favor of on-site generation. |

2026 Outlook: Data Center Orders Are the Key Signal to Watch

If data center operators continue to prioritize on-site, grid-independent power to mitigate growing energy security risks, the primary signal to watch in the next 12-18 months will be the rate of new multi-megawatt SOFC orders. A steady flow of such announcements would confirm a systemic shift in how critical digital infrastructure is powered, cementing SOFCs as a mainstream solution. The stability of regional investments, which can be affected by political shifts, remains a key factor to monitor, especially for projects in areas with high geopolitical risk.

Data Centers Are Key to Future SOFC Revenue

This chart perfectly illustrates the section’s outlook by showing a projected revenue shift driven by SOFC technology in the data center market, confirming why it’s the “key signal to watch.”

(Source: MarketsandMarkets)

- If this happens: Other data center developers and hyperscalers begin announcing multi-megawatt SOFC deployments.

- Watch this: The order books and manufacturing capacity announcements from key suppliers like Bloom Energy, Elcogen, and Ceres’ partners (Bosch, Doosan). This will reveal the supply chain’s ability to meet a surge in demand.

- This could be happening: A decoupling of data center growth from the constraints of the traditional power grid. SOFC technology would no longer be just a “clean” alternative but a “reliable” necessity for the digital economy. The success of these large projects will determine if the current momentum is a short-term boom or the beginning of a long-term structural shift.

Frequently Asked Questions

What is the main reason for the recent surge in commercial-scale Solid Oxide Fuel Cell (SOFC) adoption?

The primary driver is the data center industry’s demand for clean, reliable, and grid-independent power. This need has shifted the SOFC market from pilot-scale validation projects (2021-2024) to focused, multi-megawatt commercial deployments in 2025-2026.

Why are data centers willing to pay the high capital cost for SOFCs?

Data centers prioritize power reliability and resilience for their mission-critical operations. The high upfront cost of SOFCs is now considered an acceptable premium for securing an on-site, uninterruptible power source that is independent of an increasingly volatile and unstable traditional power grid. This makes the technology a ‘bankable’ solution for protecting digital infrastructure.

What makes the Day One Data Centers project so significant for the SOFC industry?

The Day One project, with its $2 billion+ funding for facilities including a 20-megawatt SOFC-powered data center, marks a crucial shift for the industry. It moves SOFC technology from a proof-of-concept to a primary, commercially-financed power source for critical infrastructure, confirming that investors and markets now view the technology as mature and deployable at scale.

Are SOFCs only being developed for large-scale power, or are there other applications?

While large-scale power for data centers is the main commercial driver, the application range continues to diversify. The article highlights an active innovation ecosystem with startups like Galt Tec raising funds for micro-tubular SOFCs for portable power, and Power UP Energy Technologies creating specialized power units for other high-reliability markets.

How has the main threat to SOFC adoption changed between 2024 and 2026?

Previously, a key threat to SOFC adoption was the lower cost of grid electricity. However, the SWOT analysis shows that by 2026, the threat of grid instability and geopolitical energy risks has ironically become a primary driver for SOFC adoption. The technology’s ability to provide on-site, reliable power is now a unique selling point that mitigates the threat of an unreliable grid.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.